now loading...

Sharp corrections in the equity markets and widened yield spreads arising from the emergence of the Omicron variant of Covid-19 are resulting in significant repricing risk that may impact the timetable for the US Federal Reserve’s expected bond-buying tapering.

Repricing risk is simply the possibility that assets and liabilities will be repriced at different times or amounts and affect investors’ earnings, capital or general financial condition in a negative way.

Apart from Covid-19, the low-yield environment that is expected to persist into 2022 should compel investors to be selective in their asset allocation and diversify their portfolios to focus on other assets that can deliver income in such an environment.

Before the Omicron strain surfaced, a faster tapering was expected to be announced at the December 15 meeting of the Federal Open Market Committee ( FOMC ), the Fed’s monetary policy-making body. But the ongoing market correction has made that uncertain.

“Many analysts were expecting the US Federal Reserve to announce a faster pace of tapering at the December 15th FOMC meeting. It may take two to three weeks to see the impact of the Omicron variant in terms of infection rate and hospitalization cases. This would be around the time of the December 15th FOMC meeting, potentially changing the time frame of the Fed’s tapering,” says Jim Caron, senior portfolio manager and chief strategist for the global fixed-income team at Morgan Stanley Investment Management.

In addition to the repricing risk, the Omicron variant, if it triggers prolonged lockdowns, may create more supply shortages and supply chain issues that can result in higher inflation.

“This means inflation might not be as transitory, and this would put central banks in a very tough position. If the variant turns out to be very bad, it will hurt demand and effectively prices will come down and GDP growth will be a lot slower,” says Caron.

In terms of asset allocation, Caron advises investors to be more selective on the assumption that there will be periods of volatility that provide opportunities to buy the dip. High-quality fixed income, such as investment-grade ( which has a higher duration ), could protect investors a bit, particularly in certain sectors that have been strong and are currently sold at a discount due to the recent sell-off. Asset-backed securities, which have been very expensive, have also corrected quite a bit.

“It will take the next couple of weeks to see the impact of the Omicron variant. If infection rates may not be as high as what the market feared, then market prices are going to react. The opposite is true if infection rates are higher, and this could create more of a risk-off environment. It is important to balance the portfolio with high-quality assets and find good, well-valued assets that may be sold off,” Caron says.

In the longer term, generating yield will no longer be as easy as it once was for investors in view of the economic troubles and the resulting combination of high inflation and low cash returns that are driving interest rates lower.

“While central banks are expected to move away from their ultra-loose monetary policies, prompting a rise in risk-free rates, investors are still facing very low cash return and have been driven to seek better alternatives outside of traditional sources, such as government bonds, for more yield,” says Tai Hui, managing director and chief investment strategist, Asia, at J.P. Morgan Asset Management.

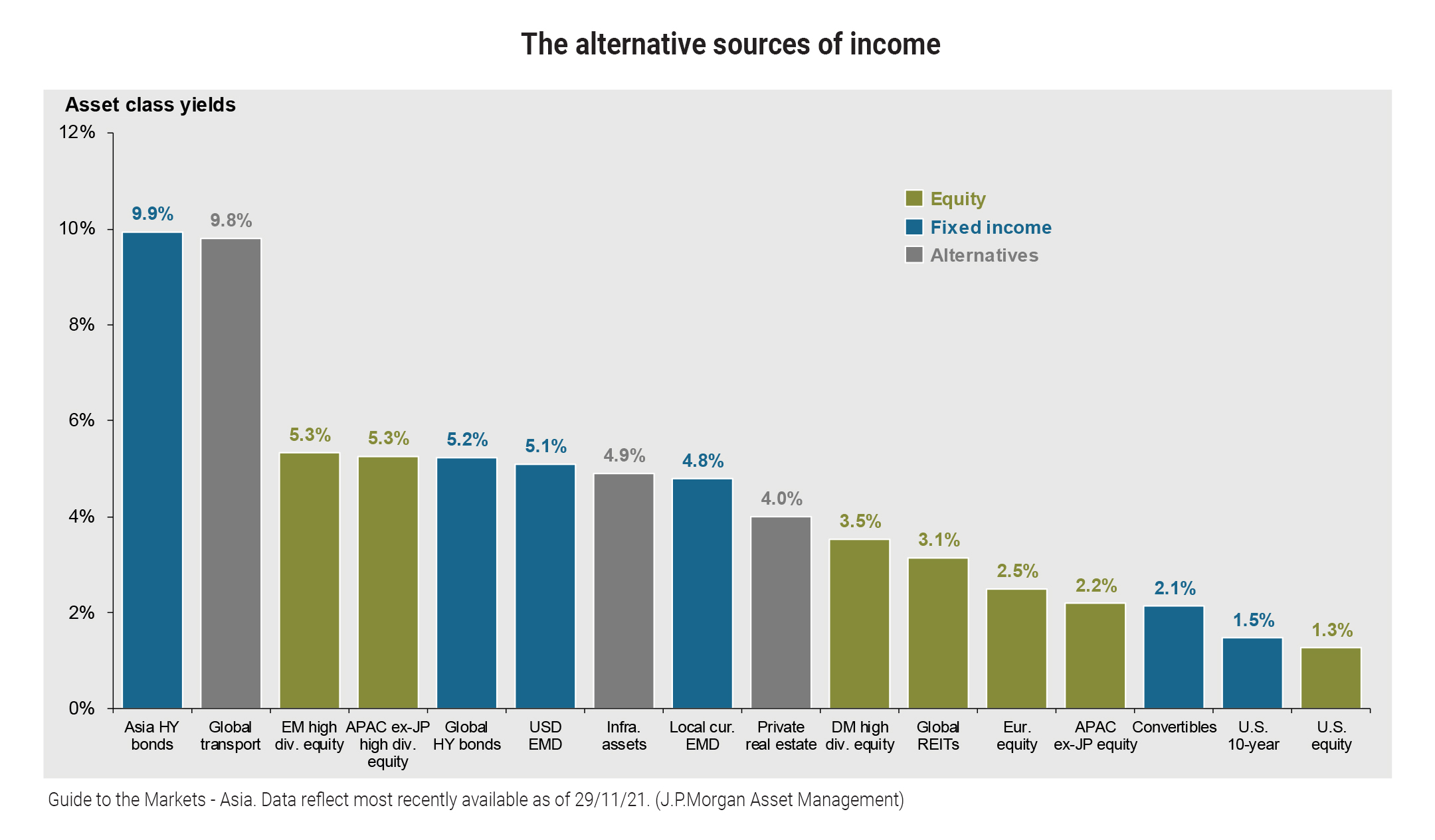

In this low-yield environment, high-dividend-generating equities, along with higher-yielding fixed income, can be a good compromise for investors seeking a steady income stream.

“The latest flattening of government yield curves around the world suggests that the market is concerned that central banks can be too hawkish and could jeopardize recovery, despite the recent surge in headline inflation,” Hui says.

Investors could also turn to alternatives for sources of yield as they have low correlation with equity markets and lower sensitivity to interest rates compared with fixed income, thus offering attractive yields. “Including alternatives as a source of income and diversification for portfolio holdings could be beneficial when market concerns over interest rate movements and economic recovery are high,” Hui adds.